For most revenue cycle leaders, bad debt has always followed a familiar rhythm…rising during periods of economic stress, easing when conditions stabilize. That rhythm is worth revisiting. The data emerging from the first quarter of 2026 does not describe a cyclical spike. It describes something more durable, and the distinction matters for how organizations structure their recovery strategies going forward. Rising hospital bad debt is no longer a temporary condition to weather, but a portfolio reality to manage.

The Numbers Behind the Trend

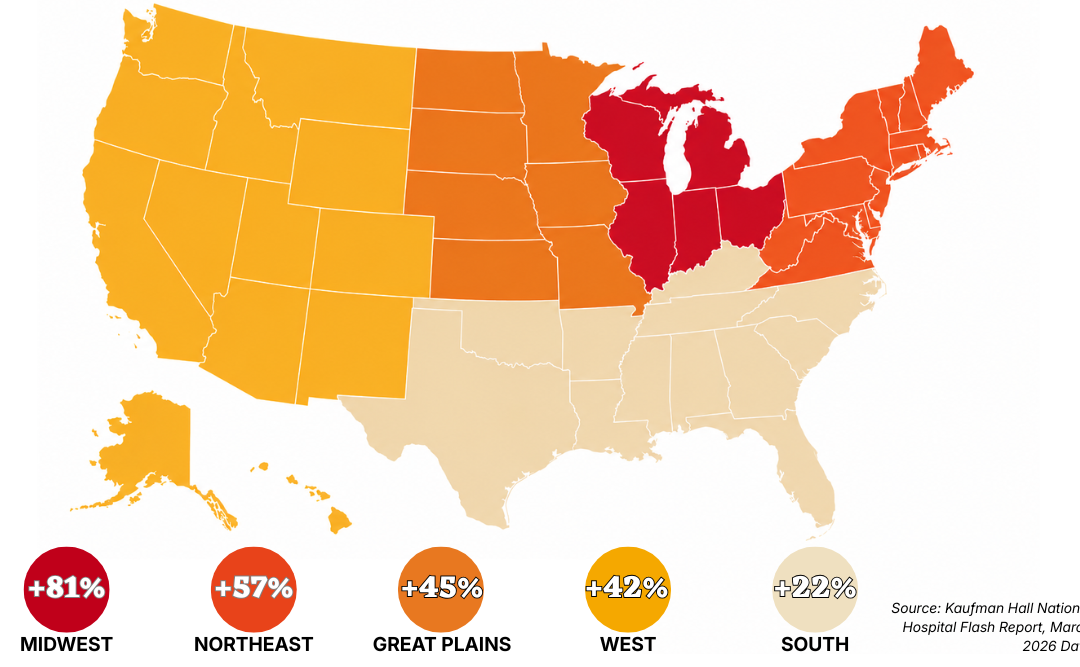

Kaufman Hall’s National Hospital Flash Report, drawing on data from more than 1,300 hospitals, reported that bad debt and charity care per calendar day rose 18% nationally in March 2026 compared to March 2025. More telling than the single-month figure is what preceded it: the first quarter of 2026 showed a sustained 15% increase year-over-year, confirming the March spike was not an outlier. Measured against the first quarter of 2023, national bad debt and charity care per calendar day has grown 46% – nearly half again as much as it was just three years ago.

The Midwest posted a 33% year-over-year increase in March, and an 81% increase compared to the first quarter of 2023 – more than double the national rate and nearly four times the growth recorded in the South over the same period. No region was spared. Every size category of hospital, from critical access facilities to large academic medical centers, recorded increases. The universality of the trend is what separates this moment from prior cycles.

What Is Driving the Surge

The forces behind this growth are not mysterious, but they are intersecting in ways that make them difficult to manage through conventional strategy alone. Medicaid redetermination (the unwinding of pandemic-era continuous enrollment protections) has left a significant share of previously covered patients without insurance. Many are now presenting for care they cannot pay for. Simultaneously, the continued expansion of high-deductible health plans is shifting meaningful financial exposure from payers to patients, a dynamic we addressed earlier this year when examining how economic uncertainty reshapes patient payment behavior well before it shows up in headline metrics.

The policy horizon adds to the pressure. The Congressional Budget Office projects that 10 million people will be uninsured by 2034 as a result of current Medicaid and ACA marketplace changes, with coverage losses beginning as early as this year. For revenue cycle leaders, the implication is straightforward: the self-pay and underinsured population is not shrinking. Organizations that treat current rising hospital bad debt volumes as temporary are likely to find themselves perpetually behind.

Managing a Portfolio That Keeps Growing

When bad debt volumes spike and recover, existing workflows can absorb the pressure. When they climb steadily for three consecutive years across every region and every hospital size, the more useful question is whether current infrastructure – staffing models, segmentation logic, vendor relationships, outreach cadence – was built for a portfolio this size. For most organizations, it was not.

That starts with segmentation. A growing portfolio is not a homogenous one. The patients entering hospital bad debt in 2026 include a meaningful share of previously insured individuals who lost coverage through Medicaid redetermination, patients who are temporarily illiquid rather than unable to pay, and patients who are genuinely facing long-term financial hardship. Each group responds differently to outreach, and treating them through a single, undifferentiated workflow is one of the most consistent drivers of preventable revenue leakage in healthcare collections.

Timing also matters more when volumes are elevated. Accounts that age unnecessarily, i.e. not because they are uncollectible, but because outreach was delayed or impersonal, represent a recoverable loss. The operational challenge in a high-volume environment is ensuring that the accounts most likely to resolve with early respectful engagement are identified and prioritized before they migrate deeper into the A/R.

The Role of Trust in a High-Pressure Environment

There is a temptation, when bad debt volumes climb, to respond with increased pressure — more contacts, more urgency, more assertive messaging. The evidence does not support this as a sustainable strategy. HFMA research has consistently shown that aggressive, non-segmented collection tactics erode patient trust and can damage long-term volume and loyalty in ways that outweigh short-term recovery gains. In an environment where patients are already under financial stress, the organizations that engage with clarity, flexibility, and genuine respect for patient circumstances consistently outperform those that do not.

This is not a philosophical position. It is an operational one. Patient engagement that builds trust produces higher contact rates, fewer disputes, more payment plan completions, and lower cost to collect – metrics that matter considerably more when the portfolio is large and margins are thin.

Closing Reflection

The Q1 2026 data makes one thing difficult to argue: the patient population driving bad debt growth is larger than it was two years ago, it is growing, and the policy environment suggests it will not shrink materially in the near term. For revenue cycle leaders, the practical question is less about whether rising hospital bad debt will remain elevated and more about whether current strategy – segmentation, outreach timing, resolution flexibility, and partner accountability – is built to perform at the volume this environment is producing. The organizations closing that gap now will be better positioned than those waiting for conditions to improve on their own.